- About

- Industry Overview

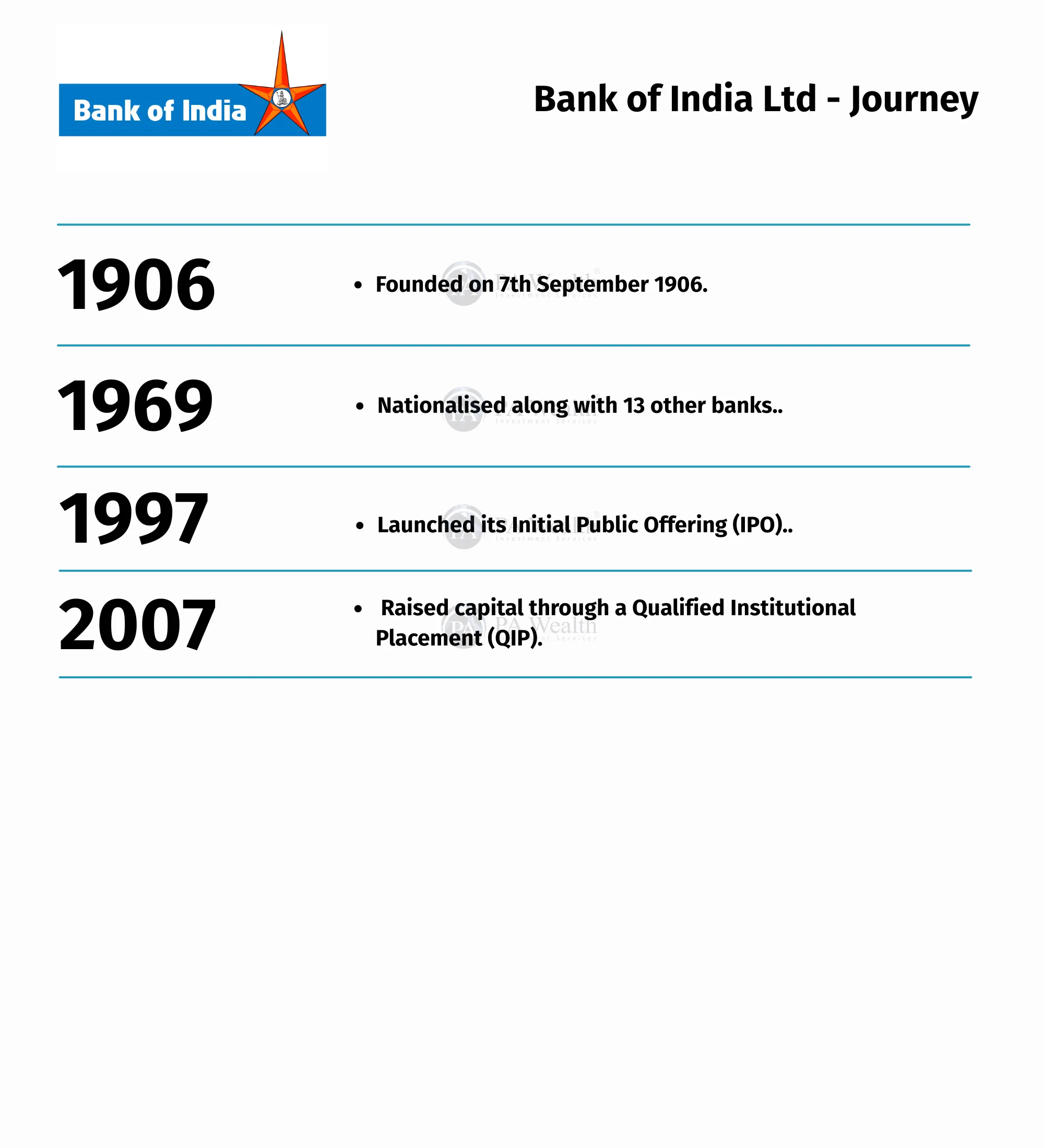

- Journey

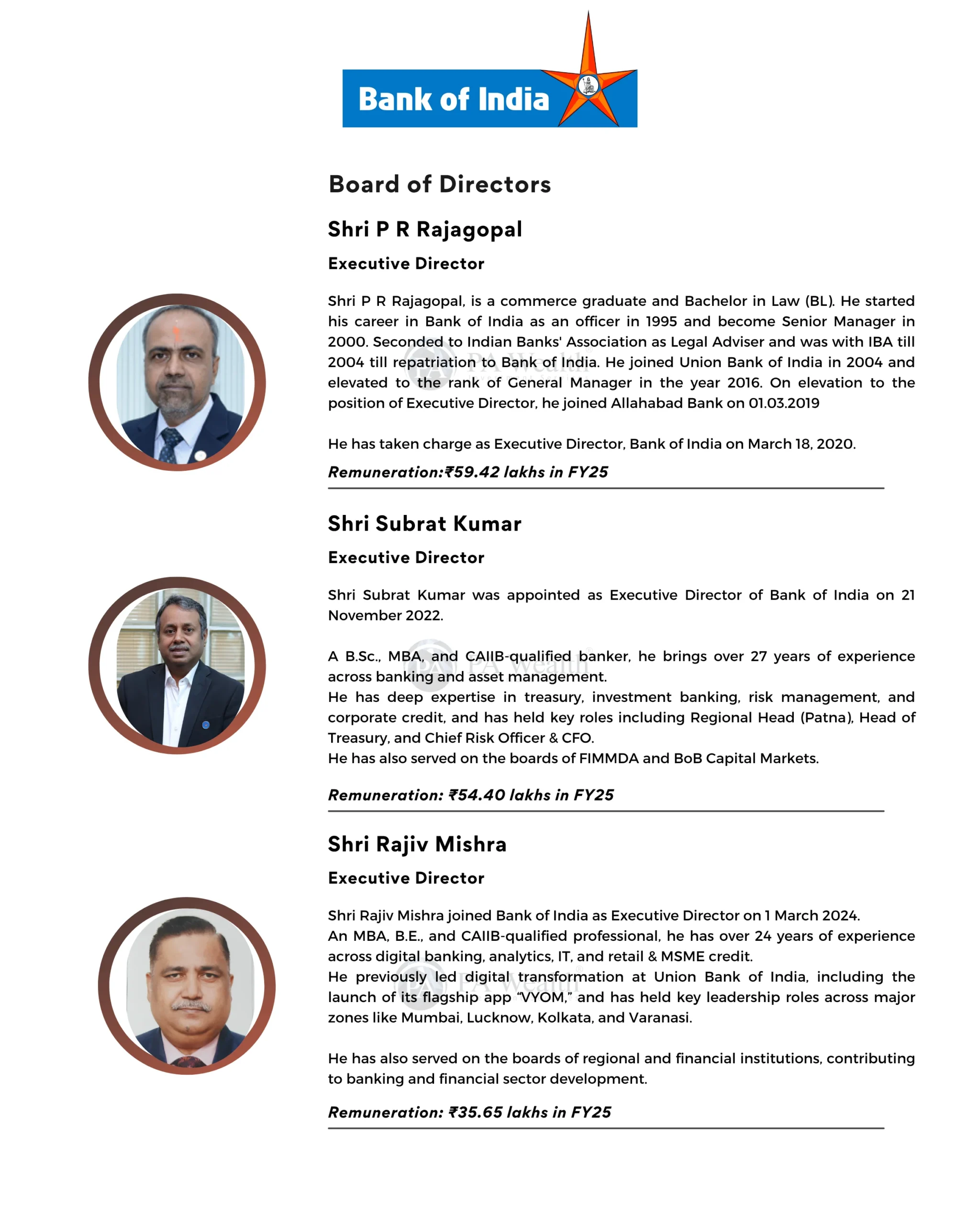

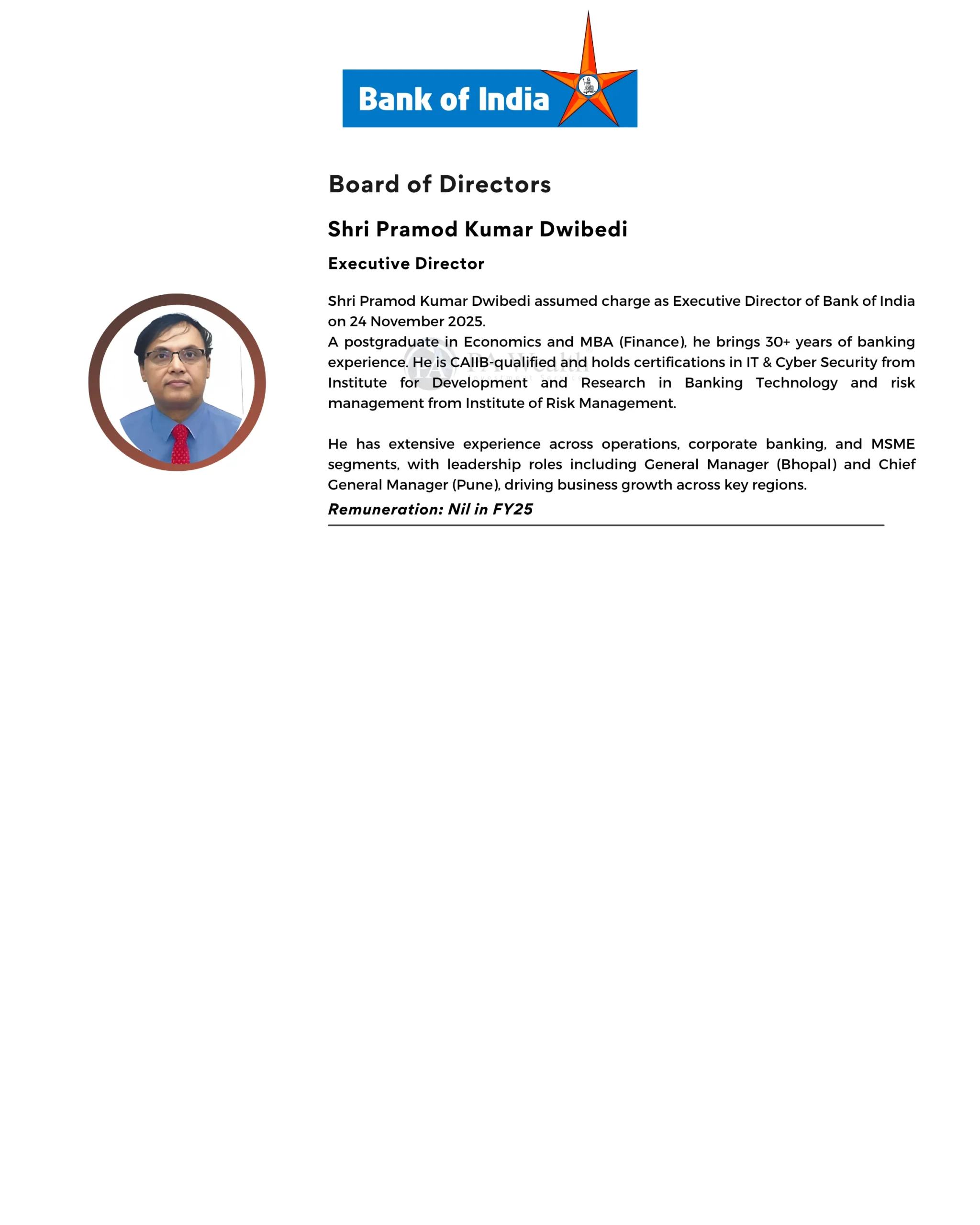

- Board of Directors

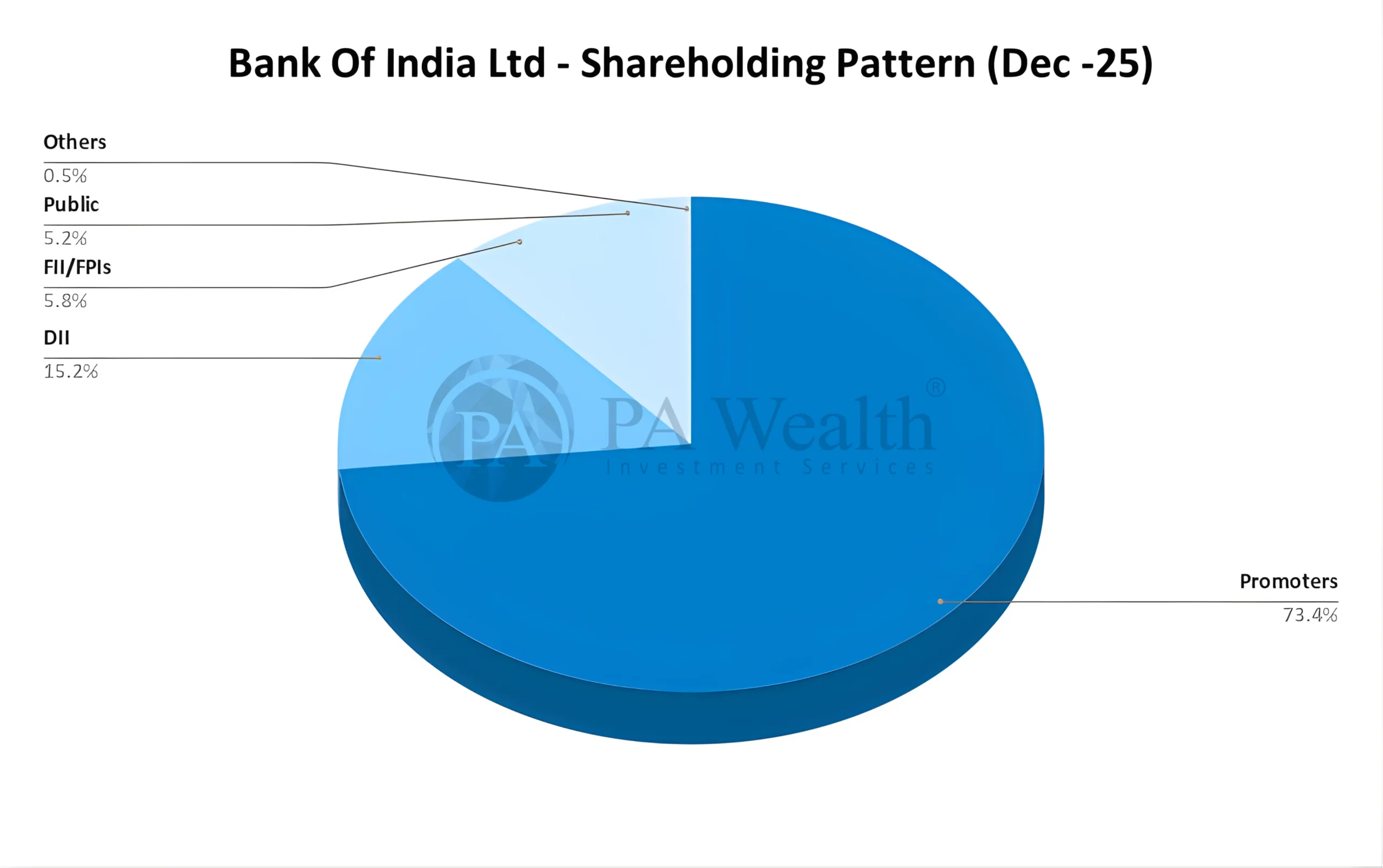

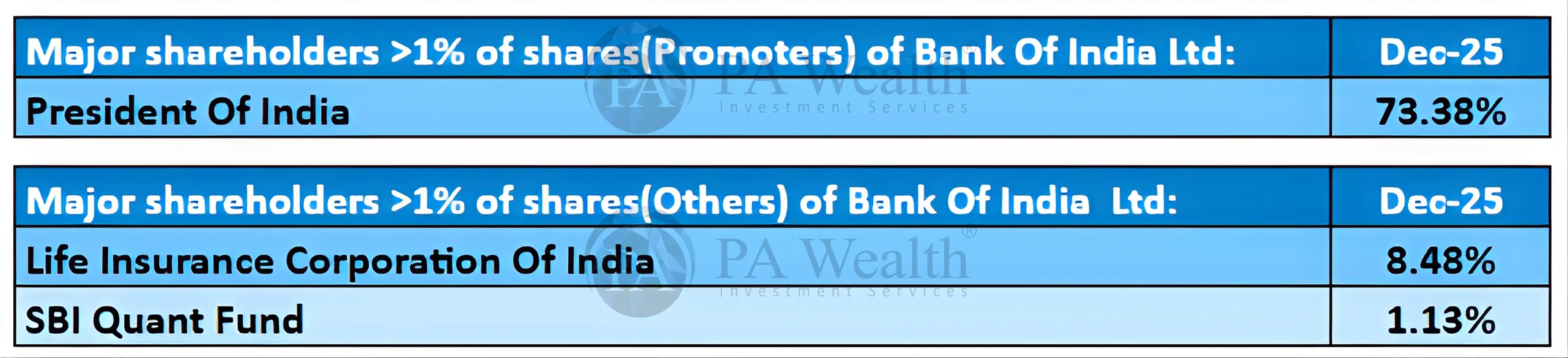

- Shareholding Pattern

- Business Segments

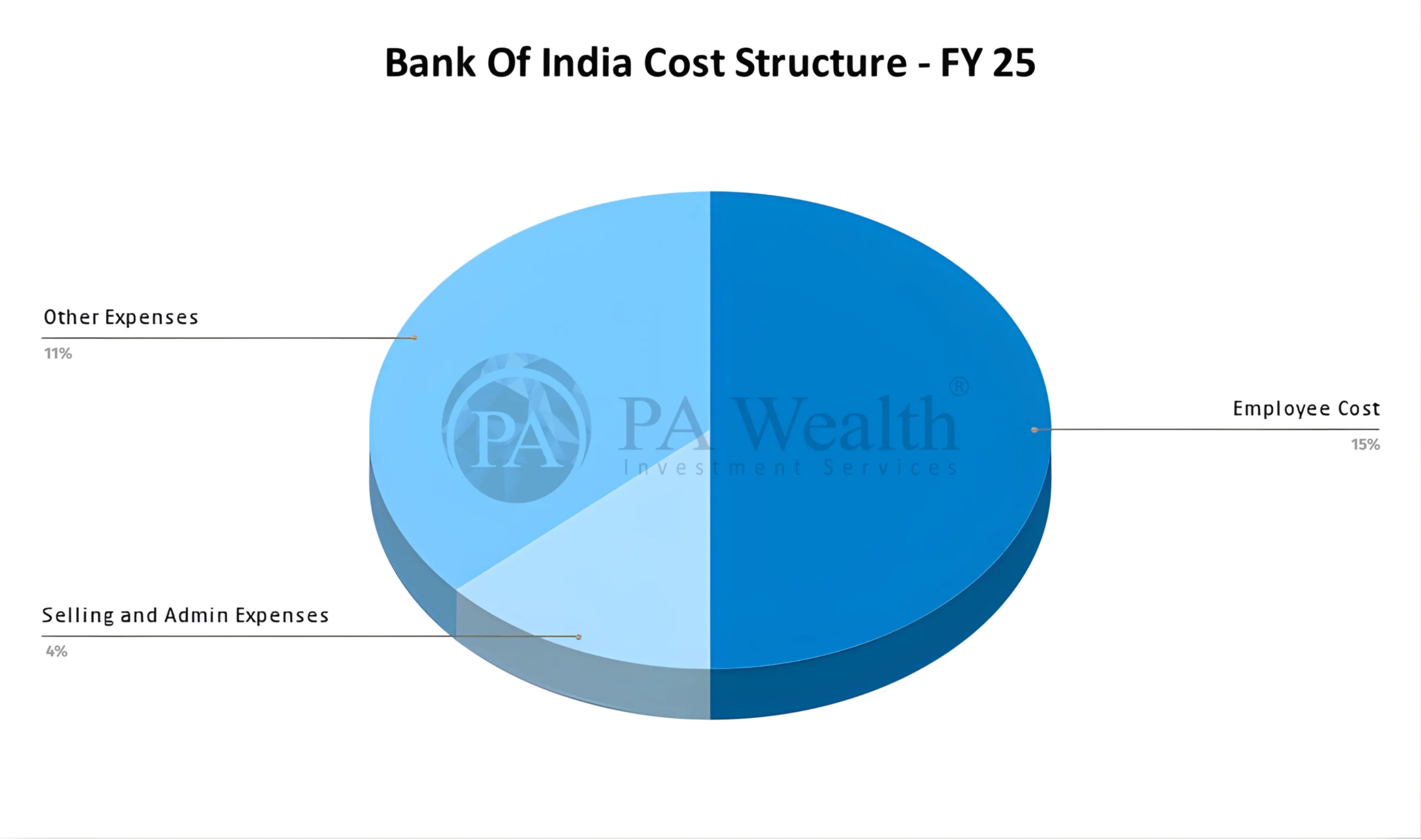

- Cost Structure

- Financials

- Management Discussion & Concall

- Strengths & Weaknesses

(A) About Bank Of India Ltd. | Stock Analysis

(B) Industry Overview

- After the global financial crisis of 2008 – 2009 Indias fiscal and monetary policies helped cushion the impact. But the following years saw a “Twin Balance Sheet problem” due to rising NPAs of the banks the and failure of payment by the corporates(Overleveraged corporates). It soon became a major economic challenge.

- yet what followed was the turining of crisis into an opportunity guided by the principle of “never waste a good crisis” in last 10 years a series of deep structural reforms began aimed to restoring the financial health and lomng term stability of the financial system.

- Now 10 years later banks are much stronger and mature than they were a decade ago and have turned the “twin Balance sheet problem” into “twin balamce sheet advantage”.

- Bank deposits and credit (domestic) have nearly tripled between 2015 and 2025, with deposits rising from ₹88.35 lakh crore to ₹231.90 lakh crore and credit expanding from ₹66.91 lakh crore to ₹181.34 lakh crore.

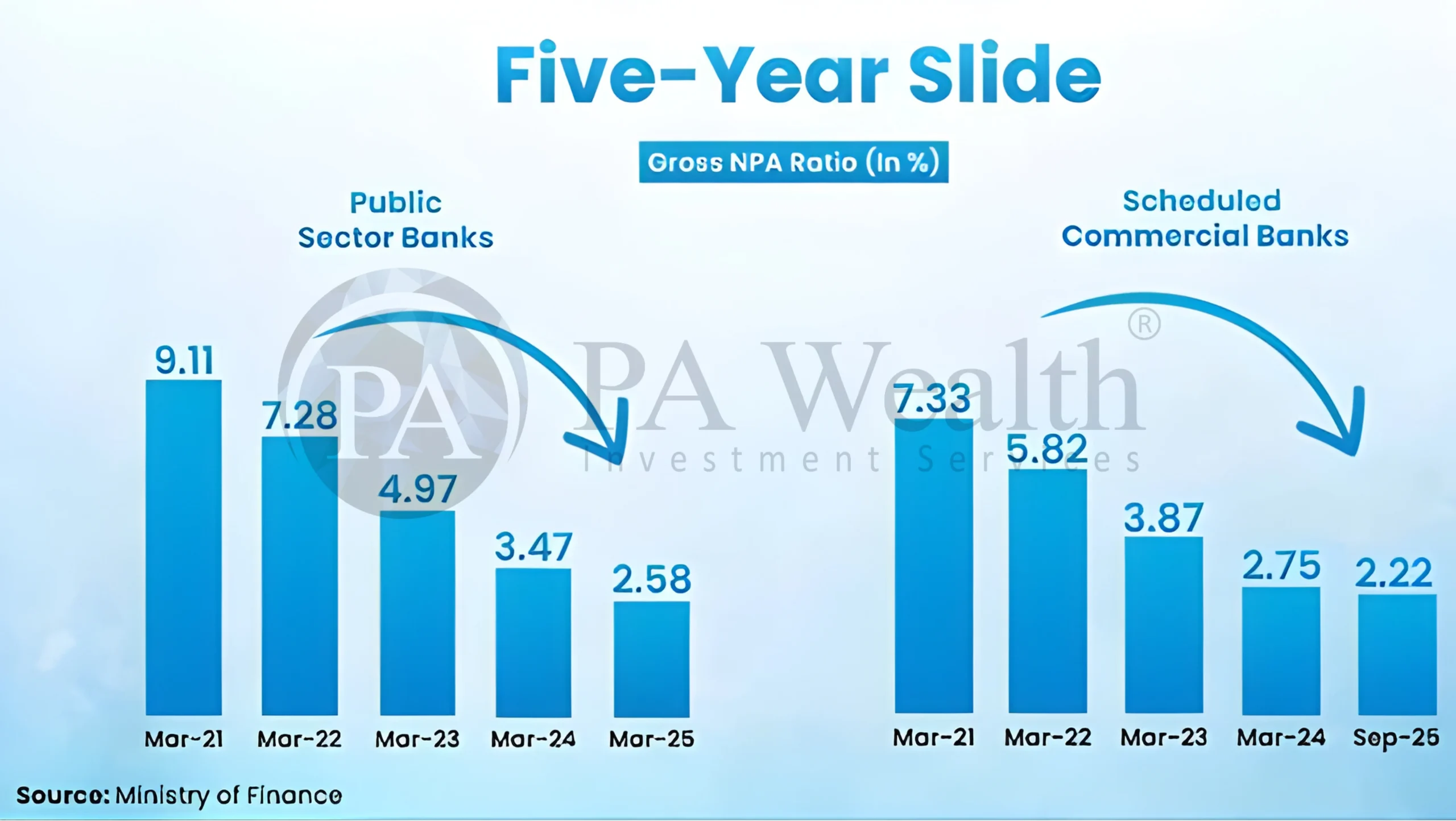

- Asset quality has also improved. Gross Non-Performing Assets (GNPA) and Net Non-Performing Assets (NNPA) have reduced to 2.2% and 0.5% in March 2025 after rising to highs of 11.18% and 5.94% respectively in March 2018.

- The Indian banking industry has seen robust growth, driven by strong economic expansion, rising disposable incomes, growing consumerism, and easier credit access. Digital modes of payments, dominated by UPI, have grown by leaps and bounds over the last few years.

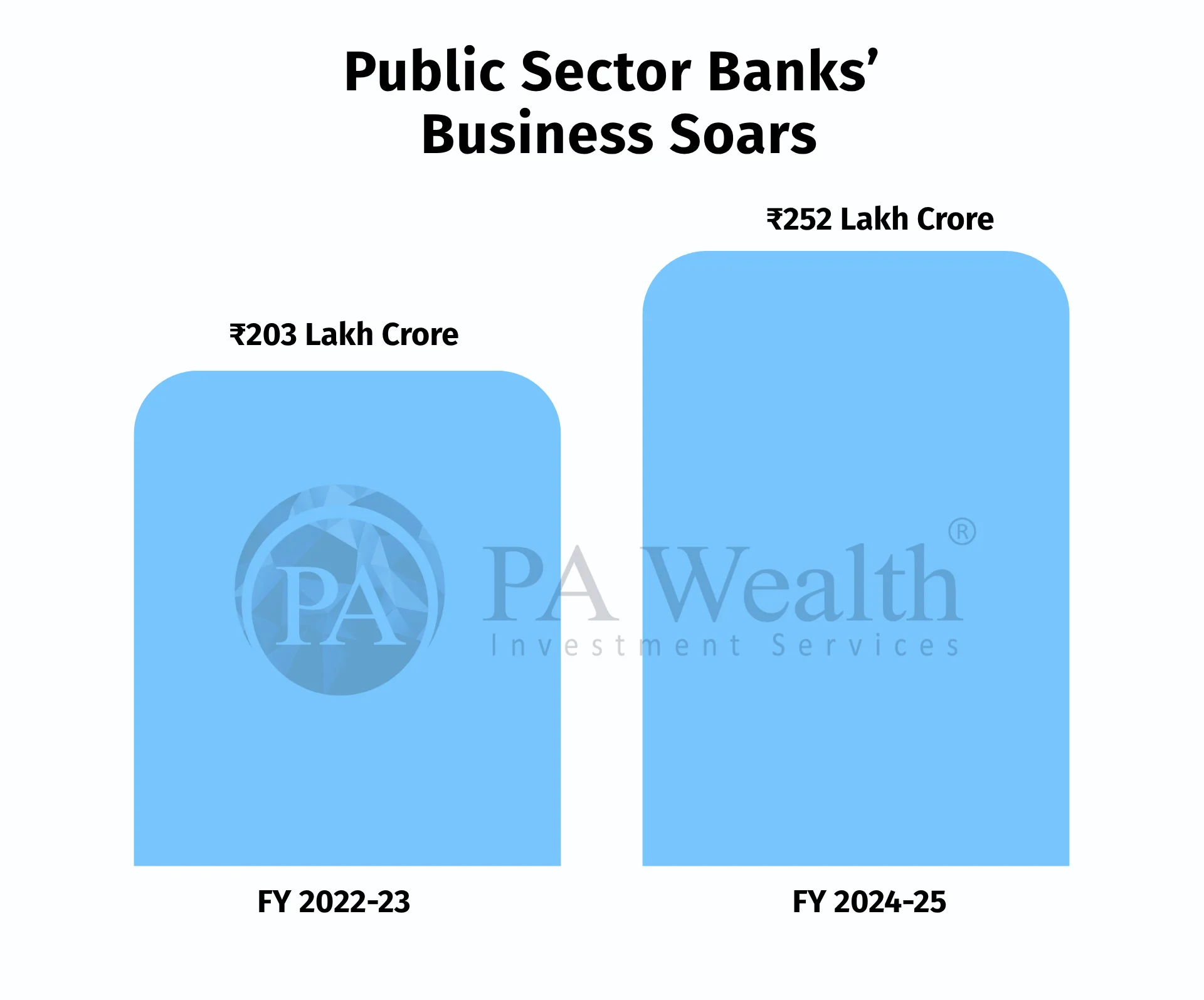

- From FY 22–23 to FY 24–25, the total Business of Public Sector Banks (PSBs) rose from ₹203 lakh crore to ₹252 lakh crore

- From FY 22–23 to FY 24–25, net profit increased from ₹1.05 lakh crore to ₹1.78 lakh crore.

- Dividend payouts grew from ₹20,964 crore to ₹34,990 crore, reflecting the continued strengthening of financial performance.

(C) Journey

(D) Board of Directors of Bank Of India Ltd.

(E) Shareholding Pattern of Bank Of India Ltd.

(F) Business Segments of Bank Of India Ltd. | Stock Analysis

1.Retail Banking Leads Growth

The bank expands strongly in retail loans.

Retail advances reached ₹1,54,207 crore.

Customers demand home, vehicle, and personal loans.

Retail segment recorded the highest growth of 20.6%.

2.MSME Segment Builds Momentum

The bank supports small and medium businesses actively.

MSME advances grew to ₹1,03,191 crore.

Entrepreneurs seek funding for expansion and operations.

This segment delivered solid growth of 15.8%.

3.Agriculture Strengthens Rural Presence

The bank continues to serve the rural economy.

Agriculture advances touched ₹1,10,844 crore.

Farmers and agri-businesses drive credit demand.

The segment grew by 16.7%.

4.RAM Segment Drives Core Business

Retail, agriculture, and MSME form the RAM segment.

RAM advances reached ₹3,68,242 crore.

This segment contributes over 58% of total advances.

The bank relies on RAM for stable and diversified growth.

5.Corporate Lending Shows Steady Expansion

The bank maintains a balanced corporate loan book.

Corporate advances stood at ₹2,60,838 crore.

Large companies demand working capital and project finance.

This segment grew at a moderate pace of 11.3%.

(H) Cost Structure of Bank Of India Ltd.

(I) Financials of Bank Of India Ltd.

(J) Management Discussion & Concall | Stock Analysis

-

During FY2025, Public Sector Banks delivered strong performance, increasing profits to ₹1.78 lakh crore with 26% growth.

-

They improved asset quality significantly by reducing gross NPAs to a 12-year low of 2.6%, supported by lower slippages.

-

As the year progressed, growth began to normalize. Credit growth slowed to around 11–12% due to tight liquidity and a high base effect.

-

Deposit growth remained moderate, especially in Q4, which created some pressure on margins and funding.

-

Despite this, the Bank maintained steady business growth. It increased deposits by over 11%, mainly driven by term deposits, while sustaining a CASA ratio above 40%.

-

The Bank expanded its advances by nearly 14%, with strong contributions from retail, corporate, MSME, and agriculture segments.

-

Retail lending led growth, especially in home and vehicle loans, while MSME and agriculture segments also performed steadily.

-

The Bank strengthened its asset quality further, reducing GNPA to 3.27% and NNPA to 0.82% through effective recovery and monitoring.

-

It also continued to expand financial inclusion through rural lending and government-backed schemes.

Growth Oulook

-

The Bank expects stable and sustainable growth, with advances projected at ~13–14% and deposits at ~11–12%, supported by a strong ₹80,000 crore pipeline.

-

Margins may face mild pressure due to repo rate cuts and high EBLR exposure, but are likely to remain broadly stable through portfolio rebalancing.

-

The liability side remains the key challenge, with CASA expected to stay under pressure due to structural changes in customer behavior and rising competition.

-

Asset quality is expected to remain strong, supported by low slippages and continued recoveries.

-

The Bank will continue focusing on RAM-led growth, higher-yield segments, and portfolio diversification to sustain profitability.

-

Ongoing investments in digital transformation, AI/ML, and automation will further improve efficiency and customer experience.

-

While external risks such as interest rate movements and deposit competition persist, the Bank remains well-positioned for balanced growth with strong fundamentals.

Q3 FY26 Concall Highlights

-

The Bank reported steady business growth, with advances up ~13.6% and deposits up ~11.6%, reflecting healthy momentum.

-

Growth was led by the RAM segment (~18%), reinforcing its role as the primary growth driver.

-

Profitability remained stable, with net profit growth (~7%) and strong operating profit (~13%), supported by a sharp rise in non-interest income.

-

Margins improved sequentially, with NIM at ~2.57%, indicating effective portfolio management despite rate pressures.

-

Asset quality stood out as a major positive, with GNPA ~2.26%, NNPA ~0.60%, and very low slippages, marking multi-year best levels.

-

The loan mix continues to shift structurally, with RAM share rising to ~58–59%, while reliance on low-yield corporate lending is reducing.

-

On the liability side, CASA declined to ~38%, with management highlighting a structural shift toward investment products.

-

The Bank continues to improve efficiency through digital initiatives, AI/ML adoption, and automation, driving productivity gains.

-

It is also expanding into new growth segments such as gig economy lending, solar financing, and premium retail products.

(K) Strengths & Weaknesses

Strengths

- Strong position among PSU banks

The bank holds a meaningful market share in loans and deposits. - Government support ensures stability

The government backing improves confidence during stress periods. - Healthy capital levels

The bank maintains capital above regulatory requirements for growth. - Improving asset quality

Lower NPAs reflect better recoveries and controlled slippages. - Reduced credit costs

Lower bad loans help improve profitability and earnings visibility. - Consistent profitability

Stable profits strengthen internal accruals and financial position.

Weaknesses

- Pressure on deposit growth

The bank struggles to grow deposits at the same pace as loans. - Declining CASA share

Lower low-cost deposits increase overall funding cost. - Loan growth outpacing deposits

This gap can create funding and liquidity pressure. - Higher reliance on bulk deposits

Bulk deposits increase risk due to higher cost and volatility. - Intense competition for deposits

Competition from banks pressures margins and deposit mobilisation.

Drop us your query at – info@pawealth.in or Visit pawealth.in

References: Annual Reports, News Publications, Investor Presentations, Corporate Announcements, Management Discussions, Analyst Meets and Management Interviews, Industry Publications.

Disclaimer: The report only represents the personal opinions and views of the author. No part of the report should be considered a recommendation for buying/selling any stock. Thus, the report & references mentioned are only for the information of the readers about the industry stated.

Most successful stock advisors in India | Ludhiana Stock Market Tips | Stock Market Experts in Ludhiana | Top stock advisors in India | Best Stock Advisors in Gurugram | Investment Consultants in Ludhiana | Top Stock Brokers in Gurugram | Best stock advisors in India | Ludhiana Stock Advisors SEBI | Stock Consultants in Ludhiana | AMFI registered distributor | Amfi registered mutual fund | Be a mutual fund distributor | Top stock advisors in India | Top stock advisory services in India | Best Stock Advisors in Bangalore